Summary

- While the dine-in aspect of restaurants faces key issues, businesses such as Dunkin' Brands, who have focused on carry-out, and delivery service only, managed to mitigate some of the impacts.

- The company has remained profitable during the pandemic, despite suffering from net store closures, reduced royalties, and rent waivers.

- Despite the risks, we believe that shares remain investable, offering double-digit expected returns, including prudent growth estimates.

- Looking for a helping hand in the market? Members of Wheel of Fortune get exclusive ideas and guidance to navigate any climate. Get started today »

Restaurants have been adversely impacted as a result of COVID-19. The sector has faced many challenges over the past few months, including closures, disrupted distribution flow, and an overall uncertainty for the future.

However, while the dine-in aspect of restaurants faces key issues, with people stuck at home, food delivery and drive-thru demand has surged. As a result, businesses such as Dunkin' Brands (DNKN), who have been able to pivot and focus towards drive-thru, carry-out, and delivery service only, were able to mitigate some of the impacts.

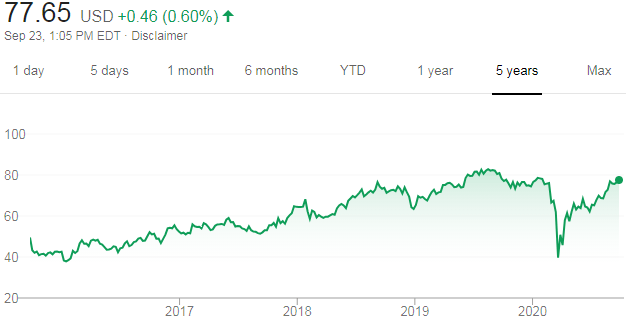

When it comes to buying struggling businesses on the cheap, however, the opportunity didn't last long. Despite shares nosediving by nearly 50% during March's selloff, the recovery was very quick, with the stock currently trading near its all-time highs.

Source: Google Finance

What we aim to answer in this article is whether at its current recovered levels, the company remains an attractive buy, or if the market has already captured much of the returns to be made.

More specifically, we will:

- Discuss the company's overall financials and prospects

- Assess the stock's valuation, capital returns, and expected investor returns

- Conclude why Dunkin' points towards double-digit expected returns, but some risks remain.

Financials and prospects

Firstly, it's important to understand the benefits Dunkin' Brands' business model merits. Because it is almost exclusively a franchised business, the company does not own or operate any of its individual locations. It is, therefore, able to focus on matters such as menu innovation, marketing, franchisee coaching and support, and the long-term success of the brand in general. The overall model is common and has the potential to be a cash cow. Financially, the franchised model allows Dunkin' to grow its points of distribution and brand recognition with limited capital investments.

The company's sources of revenue are quite the typical structure for its business model, capturing revenue streams from different ends of the overall operations. Firstly, Dunkin' charges a royalty fee, which amounts to around 5.5% of the stores' sales.

Additionally, franchisees in the U.S. pay advertising fees to the brand-specific advertising funds run by Dunkin' itself. Therefore, not only does Dunkin' not have to allocate capital towards advertising, but it can also earn some managing fees for running the whole campaign. Finally, the third major turnover stream for Dunkin' is rental income from the restaurant properties that the company leases or subleases to franchisees.