Summary

- VeriSign enjoys recession-proof cash flows, consistently improving as the demand for domain names remains stable.

- Management has been massively rewarding shareholders over the years through an aggressive buyback policy.

- Combined with ICANN's permission for price increases, we estimate double-digit investor returns in the medium term, despite minor risks.

Identifying reasonably priced companies in the tech sector can be tricky, as valuation multiples have recently expanded due to the prolonged six-month rally post the COVID-19's selloff back in late March. As stocks have been getting more expensive, dividend yields have gone down, while the massive buybacks being executed by companies are done so at higher prices, reducing their overall effect. As a result, current investors may struggle to allocate capital towards companies with enough tangible capital returns to ensure them a reasonable margin of safety.

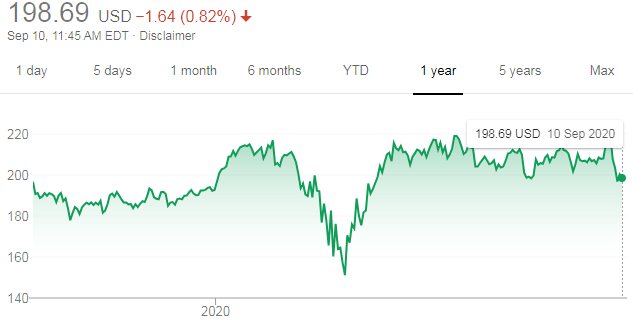

However, there are always opportunities looming, and we believe one of those lies in VeriSign (VRSN). The stock has almost fully recovered from March's initial selloff, and unlike the rest of the market, which gradually started reaching higher price levels, VeriSign's shares recovered within weeks.

Source: Google Finance

We believe that the reason for such a rush for investors to buy into VeriSign's dip is the company's COVID-19-proof business model, which guarantees robust cash flows, even under the most adverse economic conditions. Despite shares trading near all-time highs, we view the company as an attractive investment, offering consistent capital returns while having no correlation to the state of the underlying economy.

In this article, we will:

- Discuss the company's financial resiliency.

- Explain VeriSign's shareholder value creation prospects and expected returns.

- Conclude why shares offer attractive returns, despite some minor risks.

Financial resiliency

As mentioned, the company's shares returned to their pre-selloff levels incredibly quickly, as investors quickly realized that VeriSign's business model bears no correlation to the performance of the overall economy. As a result, COVID-19's adverse effects had no effect on its robust cash flows. The company is one of the few global providers of domain name registry services, essentially owning the .com and .net domain names. Because of its monopolistic qualities and the need for businesses to keep their websites running 24/7, the company's revenues are incredibly trustworthy.

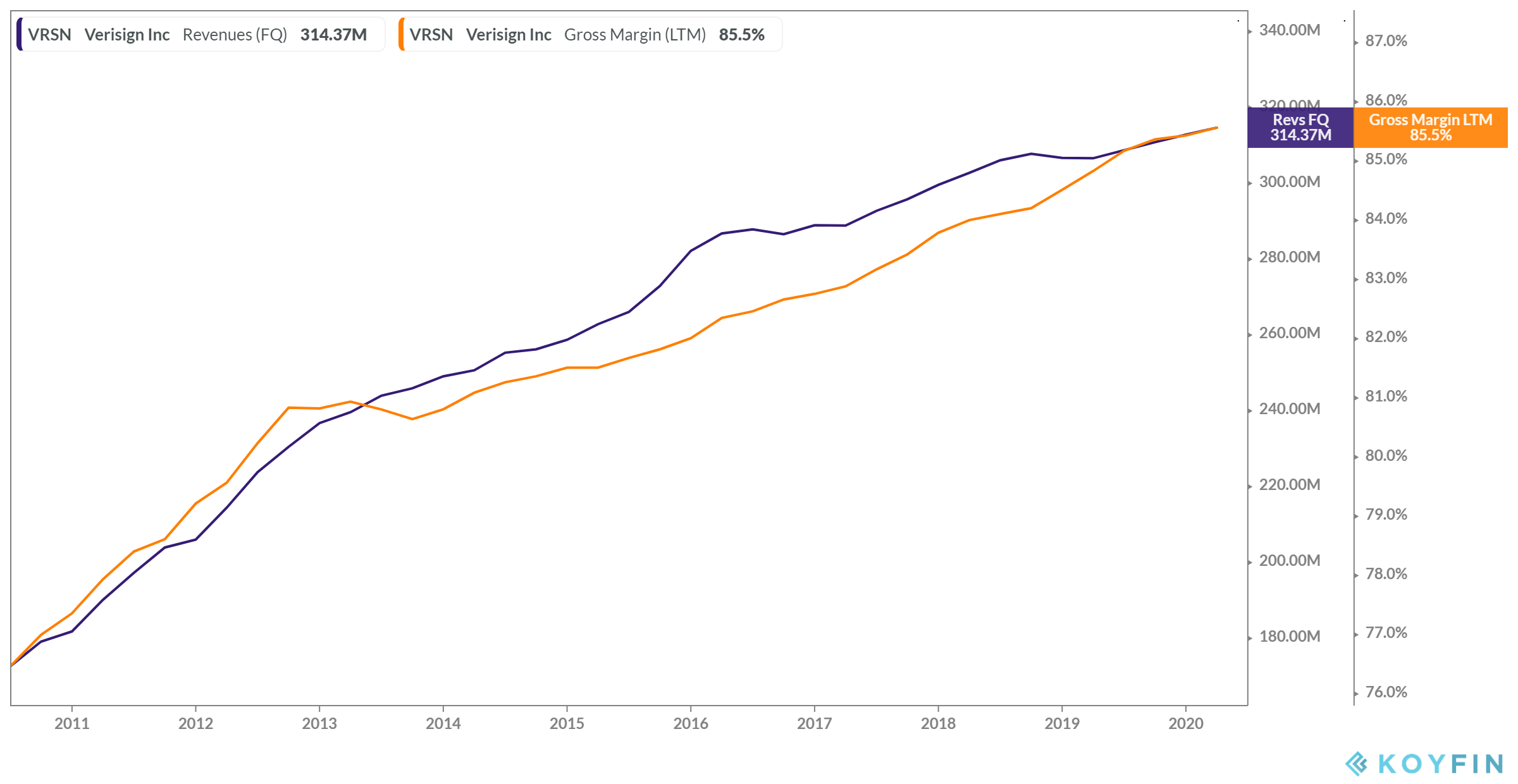

As the graph displays, despite the overall challenges concerning the global economy, VeriSign's quarterly revenues hit a new decade-high in the midst of the pandemic, reaching $314.37M. Since the company's business model is entirely passive, having relatively minor costs related to sustaining operations, its gross margins have undergone a long-term expansion path. Margins are more than likely to keep their positive trajectory as more and more names are registered to the global .com and .net networks, achieving even higher economies of scale.

The company has more than halved its workforce over the past decade, currently employing only around 872 people. With limited and consistently reduced labor expenses, VeriSign currently displays the highest net income margins (not including special cases) in the tech sector, reaching a jaw-dropping 63.3%. By focusing solely on its domain name business (e.g., VeriSign sold its security business to Neustar a couple of years ago), the company's prolonged net income margin expansion has led to consistently higher profitability. The company is pumping record levels of cash in the bank one quarter after the other.