Summary

- Dynatrace has improved its capabilities to drive sustainable growth.

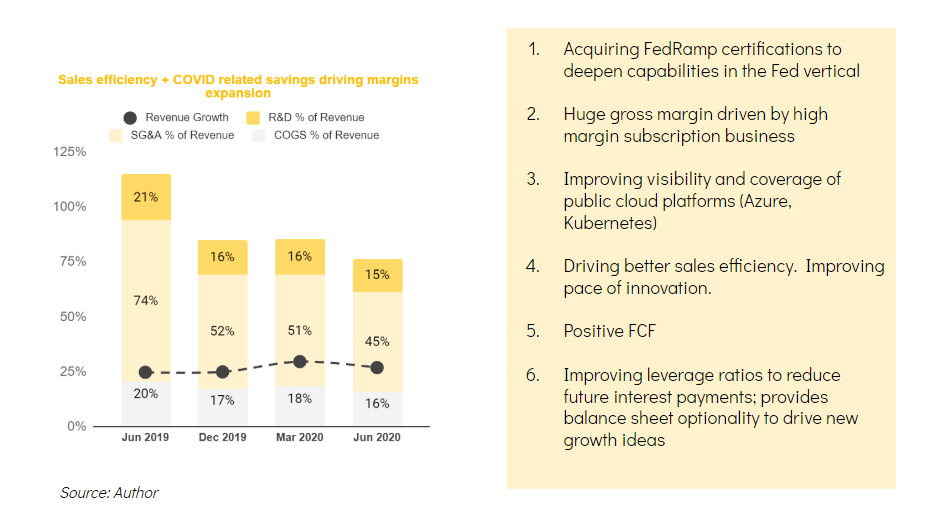

- Solid execution, improving margins and leverage ratios, and strong market positioning continues to make Dynatrace a long-term growth play.

- I am estimating FY'20 revenue of $652m and GAAP EPS of $0.31.

- The fast pace of investment to capture low hanging fruit in the DevOps space will continue to drive growth.

- I am expecting Dynatrace to exit the year at ~20x EV/FY'20.

Dynatrace (DT) remains a compelling long-term candidate to ride key tailwinds in the tech space. Dynatrace has successfully executed its transition to a subscription business. While at it, it has improved its margins and financial leverage. It is also innovating and strategizing to capture more market share as the COVID-19 dust settles. As it ramps its pipeline, Dynatrace will continue to enjoy the gains from its early start as it keeps its foot on the pedal of innovation. Given its conservative valuation ratios relative to most cloud stocks, the potential for Dynatrace to outperform is strong.

Demand (Bullish)

Stats from Dynatrace and Gartner

Dynatrace outperformed when it reported earnings last quarter. Revenue grew by 30%. This was largely driven by the subscription segment as it delivered a perfect blend of new logo and expansion wins. Digital transformation projects continue to drive the adoption of multi-cloud and scalable DevOps platforms. The thesis for Dynatrace to continue to grow market share remains strong as more enterprise projects are initiated in public and private cloud platforms. Going forward, Dynatrace is guiding for 26% revenue growth in the current quarter. This will be driven by its growing pipeline of new logos and the potential to drive more growth from its installed base. The forward growth guidance demonstrates DT's confidence in its ability to convert its near-term pipeline.

Business (Bullish)

Dynatrace is positioning for new growth opportunities in the Fed vertical.

"According to IDC, U.S. Federal digital transformation spending will reach $94 billion by 2023, with a 14.88% compound annual growth rate (OTC:CAGR) between 2020-2023."

The Fed vertical represents a significant opportunity for Dynatrace to increase its near-term monetizable TAM. Potential increase in online activities across federal and state desks buoyed the upcoming US election will also drive digital transformation activities in the Fed space.