Summary

- Investors need to focus on individual stocks to generate meaningful returns going forward.

- Prior to the COVID-19 outbreak, PVH Corp. had a strong history of profit growth.

- After falling to $48/share, PVH now trades significantly below its economic book value and at its cheapest price-to-economic book value ratio in the history of our model.

- Looking for more stock ideas like this one? Get them exclusively at Value Investing 2.0 . Get started today »

As the S&P 500 has rallied since mid-March, investors need to focus on individual stocks to generate meaningful returns going forward. This industry-leading apparel company has the cash flows and balance sheet to survive the downturn and is well positioned to grow profits during the economic recovery. Those overlooking PVH Corp. (PVH) are in the Danger Zone. Investors willing to look past the dip in economic activity can find great value in this Long Idea.

PVH Corp’s History of Profit Growth

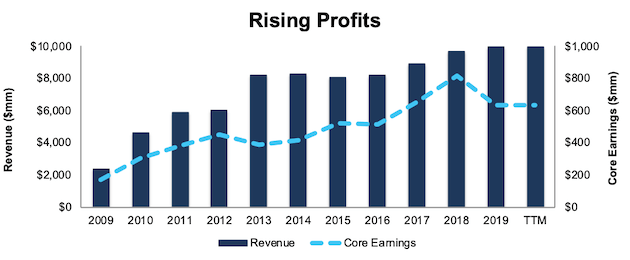

Prior to the COVID-19 outbreak, PVH Corp. had a strong history of profit growth. Since 2009, PVH Corp grew revenue by 15% compounded annually and core earnings by 14% compounded annually, per Figure 1. Longer term, PVH Corp has grown core earnings by 18% compounded annually over the past two decades. The firm increased its core earnings margin year-over-year in 14 of the past 20 years and its core earnings margin of 6% over the trailing twelve-months is up from 2% in 1999.

Figure 1: Core Earnings and Revenue Growth Since 2009

PVH Corp.’s rising profitability helps the business generate significant free cash flow. The company generated positive FCF in eight of the past 10 years and a cumulative $3 billion (67% of market cap) over the past five years. PVH Corp.’s $641 million in FCF over the TTM period equates to a 6% FCF yield, which is significantly higher than the Consumer Cyclicals sector average of 2%.