Summary

- The shares price has been up by ~120% since our first coverage last December.

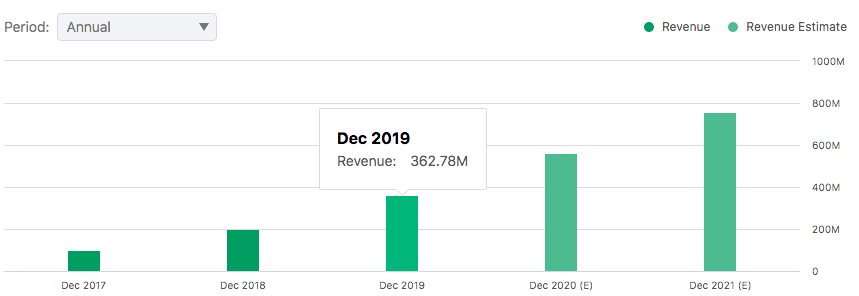

- Datadog continues to outperform. In Q1, growth accelerated to 87% YoY.

- Datadog has a high-quality business model and a highly efficient user acquisition process, which proves to drive both growth and profitability.

- The rapid product release cycle enables Datadog not only to expand its TAM but also to execute against it at a massive pace and scale.

- The stock looks overvalued at ~70x P/S, but quality does not come cheap. Datadog's resilience and consistent outperformance should drive price target to ~$112 at year's end.

Overview

We maintain our overweight rating on Datadog (DDOG), which has been on a solid run since our first coverage last December, where we discussed the company’s strong momentum in the enterprise and mid-market segments. Since then, shares price has more than doubled from ~$37 to ~$83 per-share to-date as Datadog continues its R&D investments to launch new offerings and enrich its existing ones. We expect market share gains in APM and Log Management, and growth within its Synthetics and newly-launched RUM (Real User Monitoring) businesses. Finally, the highly efficient low-friction sales model and cloud integrations should continue driving both new logos acquisitions as well as client-base expansions.

Catalyst

We expect the continuing investments in R&D and product bundling to drive TAM expansion and market share gains across APM and Log Management businesses, as well as growth across other emerging segments. Datadog stands out to us due to its capability in rapidly launching new products and features. In 2019 alone, it launched Security Monitoring, RUM, and NPM (Network Performance Monitoring) offerings along with additional features for the existing APM and Log Management offerings.

(source: seeking alpha)

In the same year, revenue grew by 82% YoY to ~$363 million. A quick look at Datadog’s blog page reveals how active it is in product developments. Impressively, these newly-launched products and enhancements quickly gained meaningful adoptions, as reflected by the solid 87% revenue growth in Q1, which represents an acceleration from ~82% YoY growth at the end of 2019.

Given the comprehensive offerings, we think that Datadog’s product bundling has been one of the key growth drivers. In Q1, 75% of new logo acquisitions reportedly landed with two or more products. The percentage of users that use at least two products has also increased from merely 32% last year to 63% in Q1. Consequently, Datadog should see more rapid growth as a result of the increasing trends in product bundling, in which the emerging offerings such as Synthetics and NPM can piggyback the success of more mature offerings such as APM and Log Management. Likewise, we expect market share gains to continue as Datadog increases its R&D investment, which has seen an increase from ~25% to +30% of revenue in the last two years.

We also believe that Datadog’s expansive cloud integration network, usage-based pricing model, and low-friction sales process will drive profitable growth longer-term. Given its self-serve onboarding model that starts with a quick sign up and free trial through its website, Datadog has a very efficient sales process.