Summary

- Dick's Sporting Goods has experienced declining operating performance in the first quarter of 2020.

- Dick's can overcome the current challenging economic environment due to its good liquidity, net cash position.

- It could be worth $41 per share by 2021.

Dick’s Sporting Goods (DKS) have been underperforming the general market since the beginning of the year. Year-to-date, Dick’s share price has dropped by 25.50% while the SP& 500 has been down by only 5.16%. In the first quarter of 2020, Dick’s has reported a declining operating performance. However, the market did not seem to care, pushing its stock price higher. Although we think Dick’s can overcome the current COVID-19 crisis due to its strong liquidity position, it is not undervalued now.

The first-quarter earnings result took a hit

In the first quarter of 2020, Dick’s generated only $1.33 billion in revenue, 30.6% lower than the same quarter last year. The comparable store sales were down by 29.5%, mainly driven by store closures along with global COVID-19 lockdown. The company had to incur additional pre-tax expenses of $62 million, including $34 million in safety and compensation and $28 million in inventory write-downs. The operating loss for the quarter came in at more than $207 million. Its loss per share was $1.71, worse than the EPS of $0.61 in the first quarter of 2019. The operating loss in the first quarter was driven by not only lower revenue but also lower gross profit. Its gross profit dropped by more than 61%, resulting from a lower merchandise margin and higher eCommerce fulfillment and shipment expenses.

The declining operating performance was mainly attributable to the COVID-19 crisis. Before March 10th, Dick’s same-store sales increased by 7.9%, and went downhill after the virus spread globally. The retailer had to close as many as 44% of its total stores. Dick’s has been trying to mitigate store closures negative impact by driving online sales. In the recent first quarter, Dick’s e-commerce sales jumped by 110%, including Curbside Contactless Pickup. The e-commerce penetration has gone up from 13% in Q1 2019 to 39% in Q1 2020. We think that the current situation is an excellent time for the company to build and sustain high growth in its eCommerce business.

It seems like Dick’s has taken most of the pain in the first quarter of 2020. Through the first four weeks of the second quarter of 2020, its consolidated same-store sales were down by only 4%. It is gradually opening stores for businesses. At the end of May 2020, Dick’s has opened up roughly 80% of its stores. As a result, we expect Dick’s operating performance would improve in its second-quarter results.

In the past year, Dick's management has implemented a lot of business initiatives, including better in-stock position and merchandise presentations, as well as rearranging floor space for growing categories. Furthermore, Dick's has exited the hunt category out of 170 stores, but delaying the plan of continuing to remove hunt products from its additional 405 stores to preserve capital. That would delay Dick's roughly $100-$120 million of restructuring expenses to 2021.

Strong liquidity position

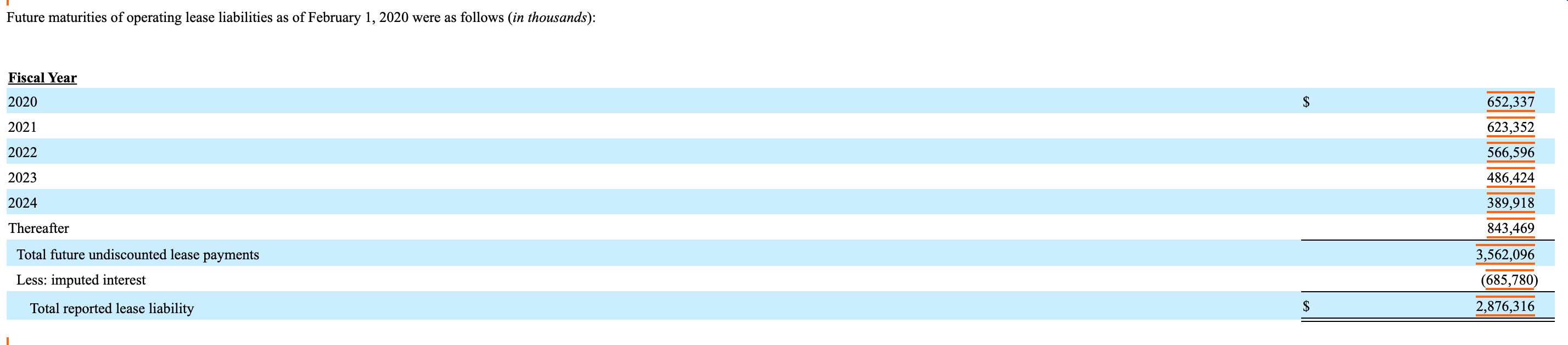

What we like about Dick’s it its strong liquidity situation. To enhance liquidity in the COVID-19 crisis, Dick’s has raised its borrowing capacity by $255 million to $1.855 billion, and issued $575 million of 3.25% convertible senior notes. Therefore, as of May 2020, it had $1.48 billion in cash and $1.83 billion in debts, including $1.43 billion in revolving credit borrowing and nearly $400 million in convertible senior notes. Besides, it has more than $505 million in operating lease liabilities and $2.43 billion in long-term operating lease liabilities. However, the lease operating liabilities maturities have spread out in many years.

Source: Dick's 10-K filing

Source: Dick's 10-K filing

In the next five years, the average annual lease payments would range from $400 million to $600 million. With the large cash balance and the average annual EBITDA of $600 million to $700 million, we think Dick’s can cover its debt and leases obligations quite easily. Furthermore, Dick's also can always renegotiate the operating leases to boost up its liquidity position if necessary.

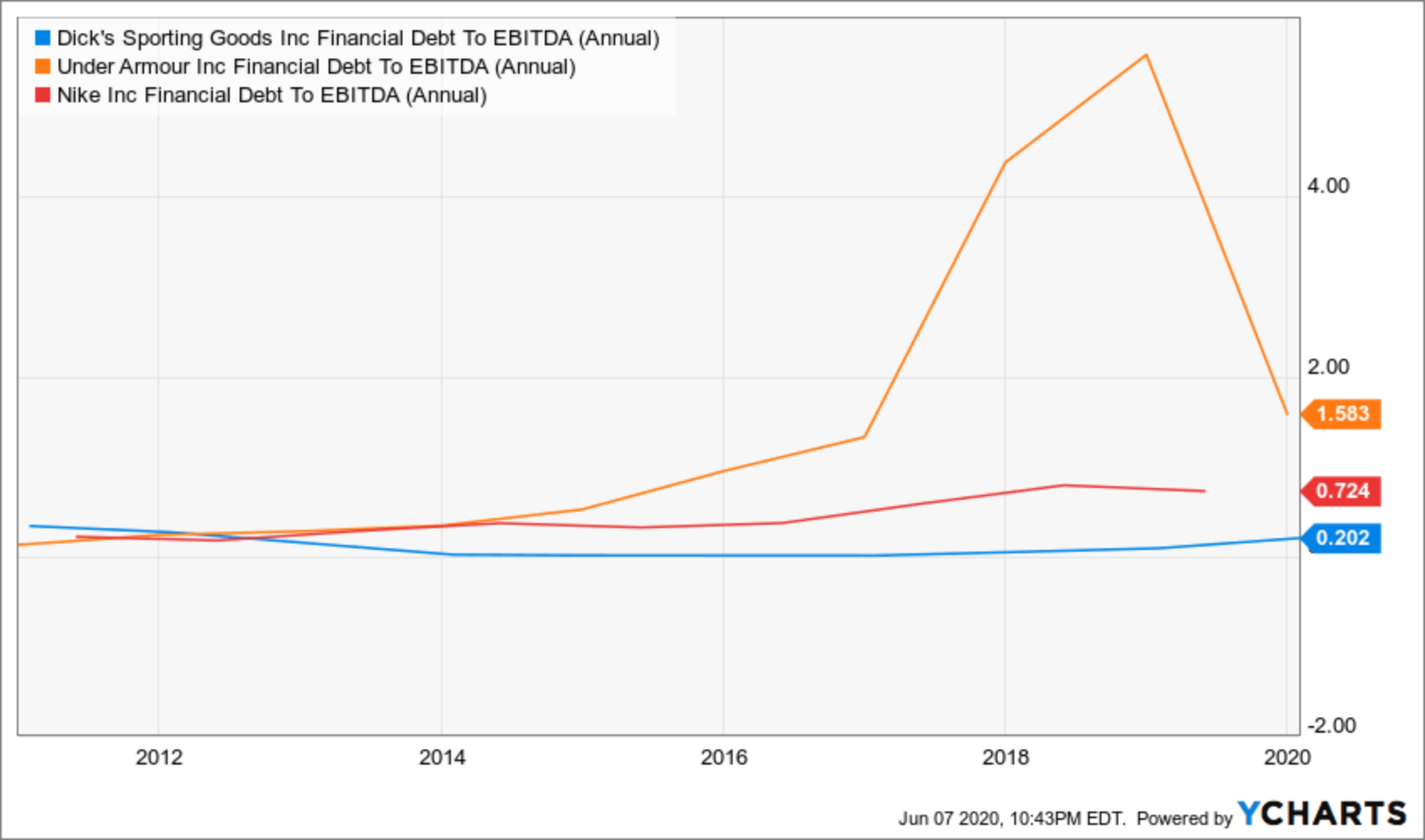

Compared to its larger peers including Under Armour (UA) and Nike (NKE), Dick's has the strongest balance sheet with the lowest leverage level.

Dick's has the lowest financial debt/ EBITDA ratio at only 0.2x while the leverage ratio of Under Armour and Nike are much higher, at 1.58x and 0.72x, respectively.