Summary

- Dynatrace's recent resurgence has been compelling.

- Besides its unattractive leverage ratios, other investing factors are improving.

- The market has priced in near-term gains, making the stock frothy to acquire.

- Regardless, I find the overall value proposition compelling if DT can sustain its growth momentum.

- I will be reiterating a Hold rating until the near-term macro headwinds subside.

Source: Author

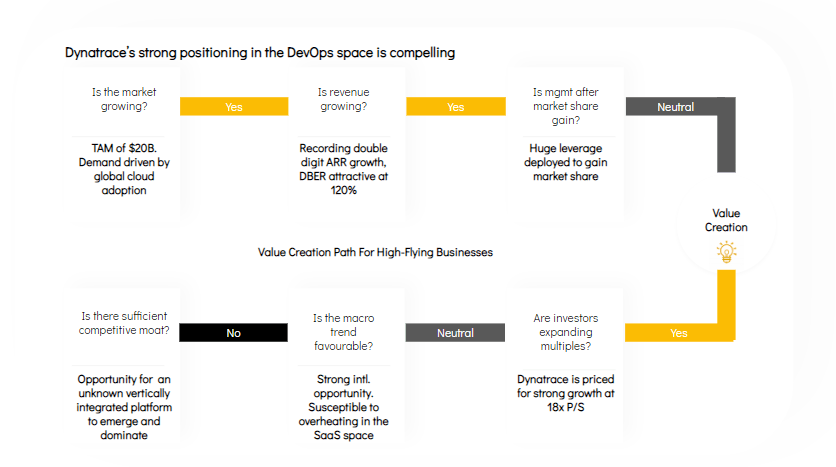

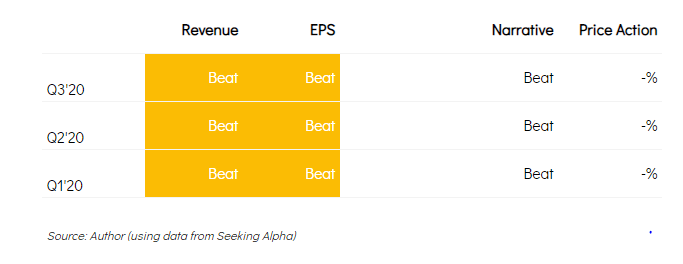

Dynatrace (NYSE:DT) reported strong growth results last quarter. The thesis for the company to keep dominating in the APM and DevOps space is intact. Favorable market trends like digital transformation and global cloud adoption have helped bolster ARR growth and strong ARR guidance, margins expansion as revenue outpaces cost, and improvement in cash flow as margins improve owner's earnings. I will be reiterating a Hold rating, though I see strong potential for more multiples expansion in the near term as more enterprises adopt DT's solutions.

Demand (Rating: Bullish)

ARR came in strong last quarter at 44% growth y/y. This was mostly driven by new customers and lesser contribution by existing expansion and migration to the new SaaS platform. Going forward, management is guiding for ARR growth of 40% to be driven by demand for its subscription and service offerings.

Dynatrace will continue to record solid growth due to its strong positioning in the expanding DevOps space. Also, the potential to cross-sell new products will drive margins. As a result, I remain bullish on the demand for DT's solutions in the near term.