- These two stocks are likely to beat earnings expectations according to our new Earnings Distortion Scores.

- One is a struggling company that looks like a good short-term play, even though long-term prospects are uncertain.

- The other is one of our highest-conviction picks that we expect to outperform in both the short and long term.

- Looking for more stock ideas like this one? Get them exclusively at Value Investing 2.0 . Get started today »

General Electric (GE) and Lam Research (LRCX) are this week’s Long Ideas.

These two stocks are likely to beat earnings expectations according to our new Earnings Distortion Scores. One is a struggling company that looks like a good short-term play, even though long-term prospects are uncertain. The other is one of our highest-conviction picks that we expect to outperform in both the short and long term.

We measure earnings distortion using a proprietary human-assisted ML methodology. Street earnings estimates are incomplete and less accurate since they do not consistently and accurately adjust for unusual gains/losses buried in footnotes. By adjusting for earnings distortion, we create a measure of core earnings that is more predictive of future earnings.

We'll be highlighting the Earnings Distortion scores for the important earnings releases for the following week. Our goal is to help investors combat increasingly material levels of earnings distortion. Earnings for the S&P 500 were distorted by an average of 22% in 2018, and we expect that trend to continue.

Earnings Distortion Highlights

Earnings season won’t get into full swing until February, but there are still plenty of stocks that report earnings in January. Of those stocks, LRCX and GE both stand out for their negative earnings distortion – i.e. their reported GAAP earnings are below their recurring core earnings.

Figure 1: Two Stocks That Should Beat Expectations – LRCX and GE

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filingsAlthough we expect both stocks to beat expectations, our long-term outlook for the two companies is very different.

Lam Research (LRCX)

We first made Lam Research a Long Idea on May 23, 2018 in our article, “This Pick and Shovel Stock is Still a Value.” Since our article, LRCX has outperformed the market, up 43% vs. the S&P 500 up 17%.

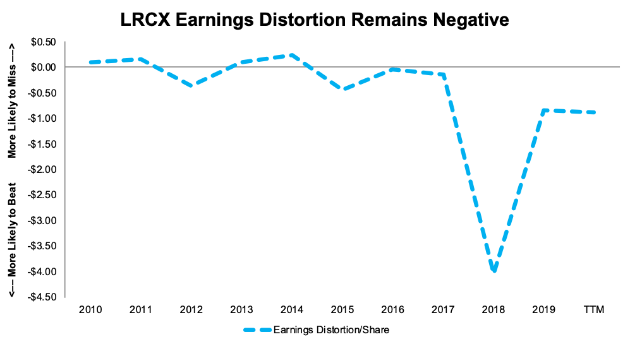

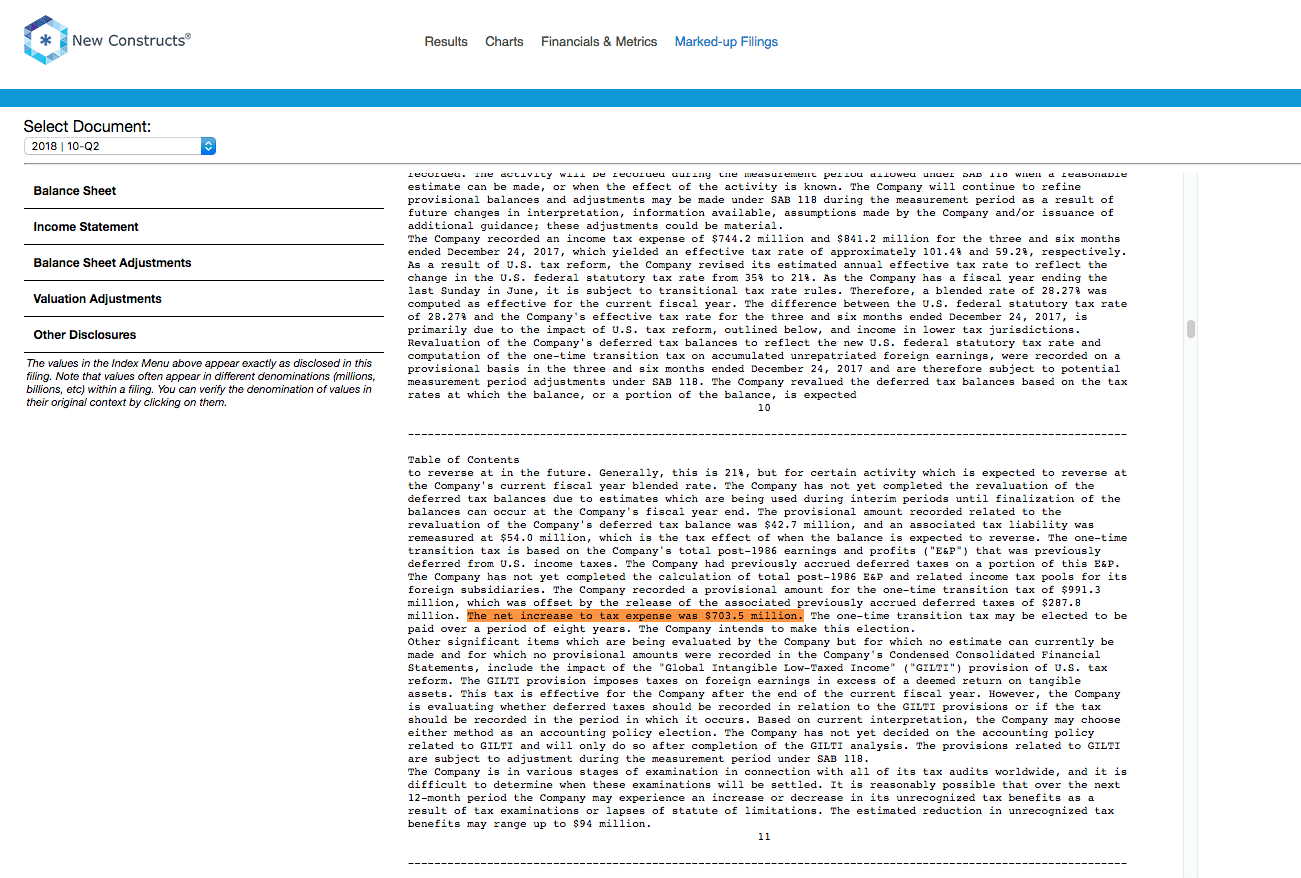

In our original article, we noted that LRCX’s GAAP net income at the time was significantly understated due to a $704 million (6% of total assets[1]) non-recurring charge related to the corporate tax cut. This non-operating charge led to LRCX’s GAAP net income understating its core earnings by $4.04/share in 2018, as shown in Figure 2.

Figure 2: LRCX Earnings Distortion/Share: 2010-TTM

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filingsMost sophisticated investors likely understood that the tax law would have a big impact and were on the lookout for unusual tax charges in 2018. However, many investors probably don’t realize that companies continue to face non-recurring tax charges as they update their estimates for the impact of the tax law.

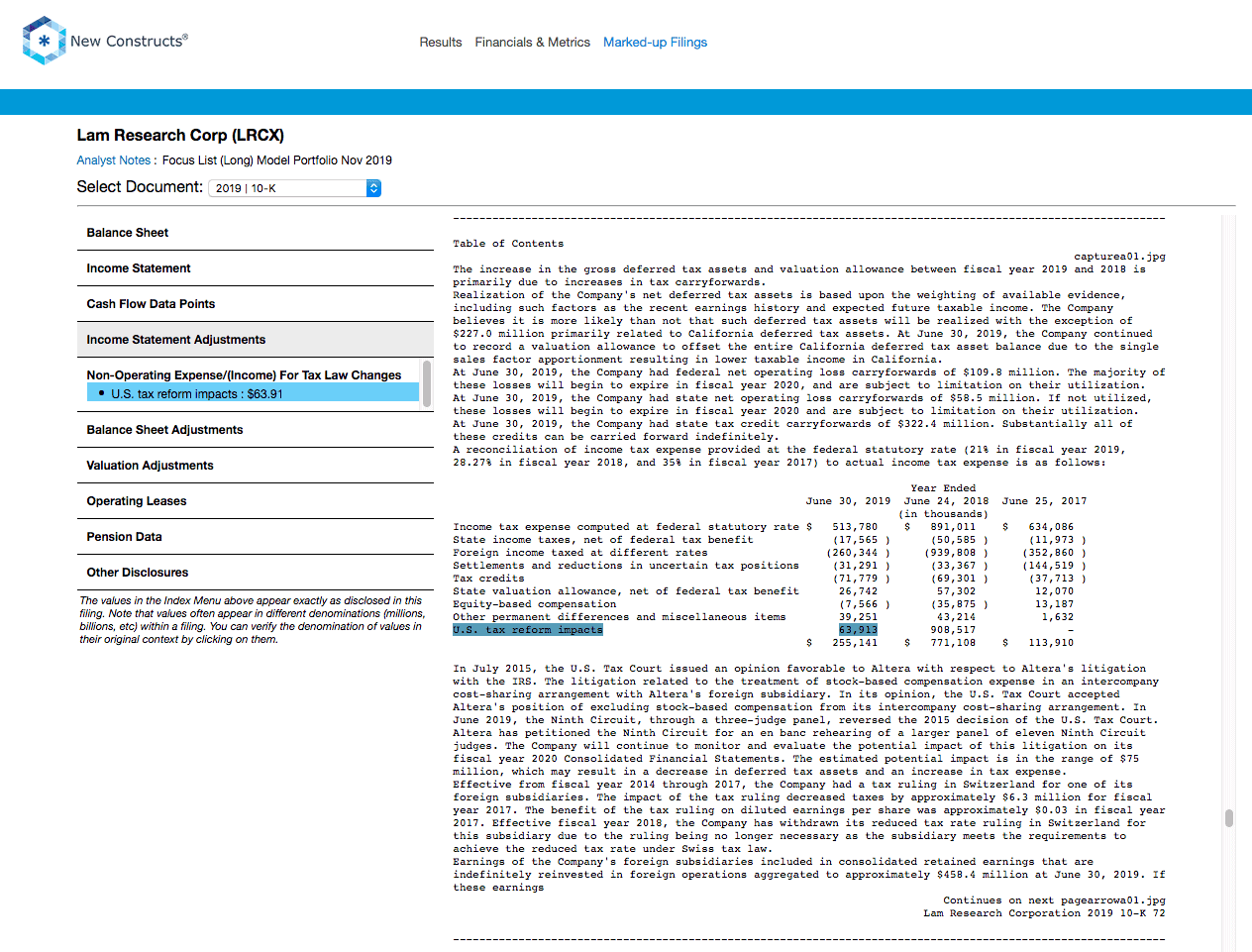

In 2019, LRCX disclosed a $64 million (<1% of assets) tax charge as a result of U.S. tax reform.

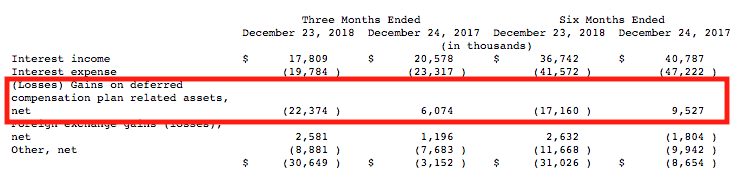

Increasing the likelihood that LRCX beats earnings expectations, its comp for the upcoming quarter – 2Q 2020 – should be especially favorable. In the year ago quarter, the company disclosed a $22 million loss on deferred compensation plan assets.

Taken altogether, the TTM earnings distortion for LRCX totals -$139 million (1% of assets). On a per share basis, earnings are understated by $0.89/share, or 23% of consensus earnings estimates for Q2. Given this level of earnings distortion, LRCX looks well set up to beat expectations when it reports earnings on Jan. 22.

{kind=link}

{kind=link}

{kind=link}