Summary

- Datadog delivered strong growth numbers last quarter.

- The company's valuation is leading its future growth projections.

- Its offerings in APM and log management improve its value proposition to customers.

- At a P/S (ttm) of 33x, the stock is no longer a bargain.

- I will remain on the sideline, as I find Datadog's products attractive to establish a position in the event of a correction.

Datadog's (DDOG) valuation will continue to lead its growth narrative in the near term. The robust product pipeline and global expansion initiatives will continue to attract growth investors. Given the lofty sales multiples, which is currently above its peer and sector average, Datadog will have to beat and raise growth guidance consistently. This makes the stock susceptible to a downward knee jerk reaction in the event of an earnings miss. As a result, I'll prefer to wait for a correction before acquiring a position.

Source: Forbes

Demand (Rating: Bullish)

The APM market is one of the largest subsegments of the ITOM market, with a 2019 preliminary forecast revenue of approximately $4.1 billion and a growth rate exceeding 10% CAGR through 2022. - Gartner

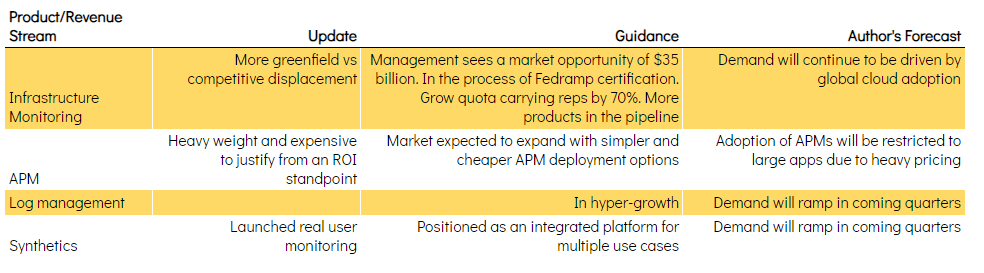

The demand for Datadog's solutions remains strong, and the impressive results from last quarter highlighted this. Revenue grew by 88%, while ARR (deals greater than $100,000) improved by 93%. This highlights the strengths of Datadog's solutions. Dollar based net retention rate was slightly over 130% as Datadog benefits from cross-selling new products. The company is in the process of FedRAMP certification to expand its strengths in the Fed vertical. Management is guiding for more product updates and releases. As a result, I remain bullish on Datadog's growth potentials in the near term as the global transition of workloads to the cloud will continue to drive the demand for Datadog's products.

Business/Financials (Rating: Bullish)

Source: Author (using data from Seeking Alpha)

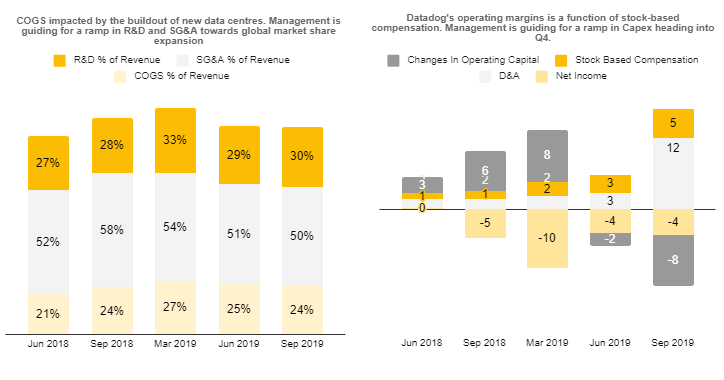

During the last conference call, management shed some light on its robust product pipeline. Also, management is guiding for an increase in operating expenditure to pursue more growth both locally and internationally. This revolves around adding more products and features, adding to sales capacity, and investments in cloud assets.

Source: Author (using data from Seeking Alpha, data in millions of USD)

While this means Datadog is expected to maintain its negative operating and profit margin in the near term, the aggressive pursuit of growth is a sign that there is a strong opportunity to expand market share. Unlike a lot of SaaS plays, Datadog's profit margins aren't too bad. The company has been able to improve sales efficiency as more large enterprises adopt its products. Going forward, I expect this trend to continue as more customers adopt more than one product. If margins continue to improve, Datadog's ability to generate positive free cash flow will improve as well.

Datadog has a strong cash position, and the current balance sheet is healthy, given its debt to equity ratio of 8% and a current ratio of 4.9.

As a result, I remain bullish on Datadog's business and financials in the short term as the ample cash position ($771m) gives management the leeway to unlock more value.