- HubSpot's strong positioning within the mid-market segment and its overall low-touch user acquisition strategy will continue to drive long-term growth and margin expansion.

- Despite the downside Q4 outlook, Q3 revenue growth of ~32% YoY and guidance beat have overall been convincing.

- HubSpot is at the early stage of its transformation into a full CRM suite. Much of the upsides are yet to be realized.

Overview and Q3 review

In the SaaS CRM sector, HubSpot (HUBS) has stood out as one of the few competitors with a solid freemium user acquisition strategy. HubSpot is the pioneer of inbound marketing concept, which relies primarily on quality content marketing to drive conversions into paying users. Since it started, HubSpot has been leveraging its own technique to market its CRM product to the mid-market segments globally.

We hold a bullish view on HubSpot. Looking at its recent performance as of Q3, we are confident in HubSpot's user acquisition strategy, which we think fits its product roadmap and target market segment perfectly. HubSpot's $167.1 million subscription revenue beat its Q3 guidance, though its professional services revenue of $6.5 million fell below the estimates. Overall, HubSpot grew its customer base by 31% YoY to 68,803.

Working freemium and transformation strategies to serve the mid-market CRM demands

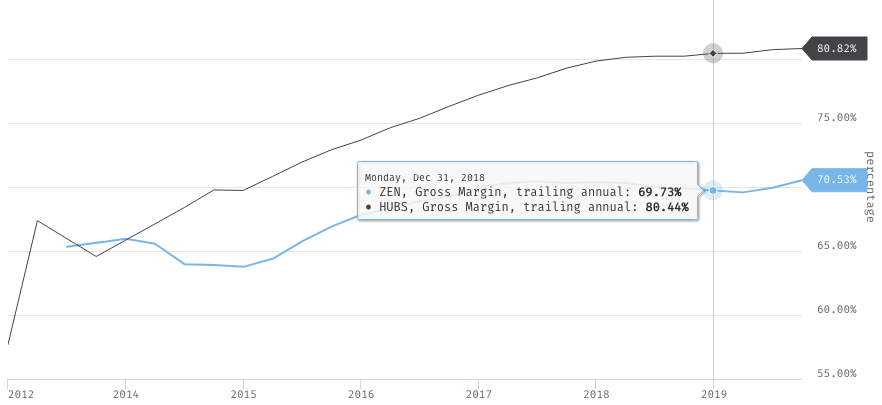

(source: stockrow. Zendesk vs. HubSpot gross margin)

With fewer resources required to support its users' onboarding due to its low-touch freemium strategy, HubSpot can incur a lower cost of revenue. Ultimately, the strategy resulted in ~8 - 10 PPS higher gross margin when compared to other SaaS CRM players like Zendesk (ZEN). In the last few years, HubSpot has also become more efficient in its approach as it expanded its gross margin to widen the gap with Zendesk.