Summary

- HubSpot will continue to benefit from the demand for marketing and sales automation tools.

- Improving profitability margin will also help drive cash flow.

- Regardless, investors should be wary of buying at an expensive valuation.

- I rate HubSpot a HOLD, and a buy at $130/share.

HubSpot (HUBS) is a volatile stock enjoying strong growth momentum in the SaaS space. Demand for marketing and automation solutions in the United States and globally, coupled with HubSpot's thought leadership, will continue to propel sales momentum in the near term. Due to the improving profit margin, it will be tough to pass on HubSpot at its current valuation. At a P/S of 11X, HubSpot is not cheap. Regardless, I'll be a buyer if shares fall to $130 (forward P/S of 7x).

Demand

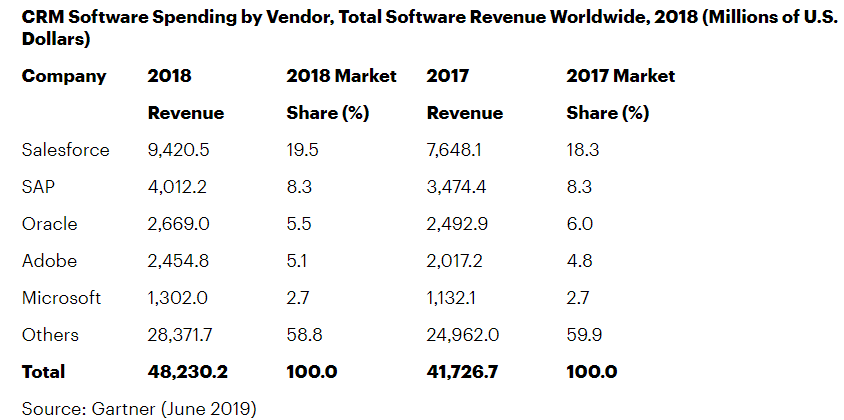

Source: Gartner

Worldwide spending on customer experience and relationship management (CRM) software grew 15.6% to reach $48.2 billion in 2018, according to research from Gartner, Inc. CRM remains both the largest and the fastest-growing enterprise application software category.

Demand for CRM tools is now primarily driven by SaaS and cloud deployments. HubSpot plays in the marketing subsegment of the CRM market, which represents 25% of the overall market. It is also the fastest-growing segment expanding by 18.8% y/y.

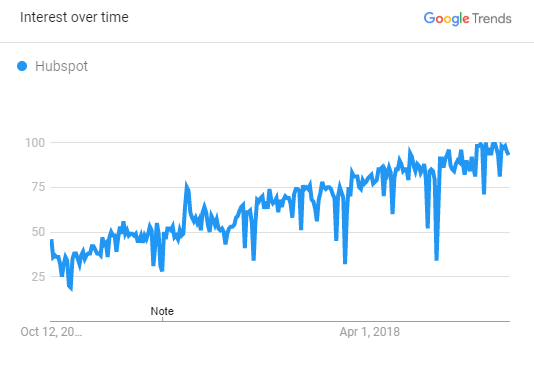

Source: Google

HubSpot has been able to distinguish itself from the myriads of CRMs out there via its thought leadership in inbound marketing. According to a consumer survey conducted by the company last year, 26% of respondents first learned about HubSpot via Google (GOOGL). As the chart from Google Trends above portrays, HubSpot has grown in popularity over the past five years.