Summary

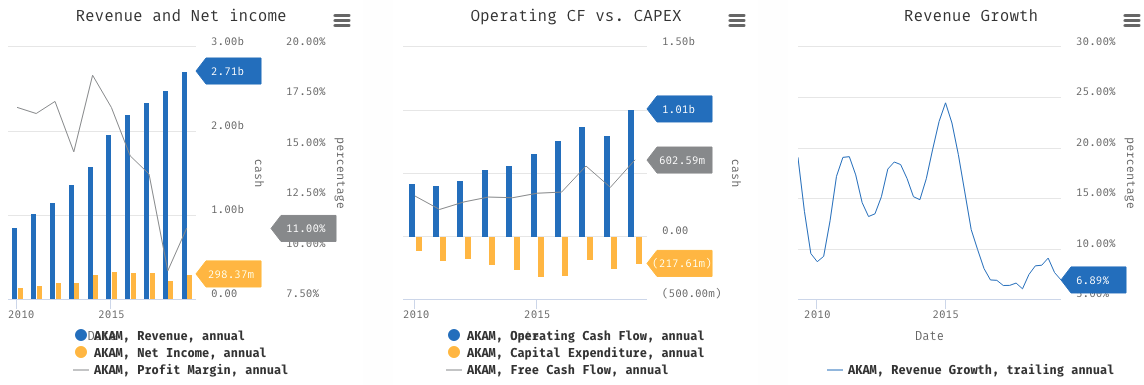

- Akamai is a technology stalwart. It recorded $2.71 billion of annual revenue last year, growing at 6.89% TTM, and has been consistently profitable much all of its entire operating history.

- Its core CDN business has hit a saturation level, with growth of only 1% to 2% seasonally at best.

- Its progress in relatively new enterprise Cloud Security segment has been promising. Last Q2 2019, we learned that this segment makes up almost 44% of all Akamai's revenue so far.

- Looking at its competitors in the space like Okta or F5, we think Akamai will double up in share price to trade closer to these competitors in next two years.

Overview

Our thesis is long Akamai (NASDAQ:AKAM). To us, it is one of the stalwarts of the technology industry. Despite the maturing enterprise CDN market where the growth is relatively flat YoY, we think that Akamai's recent move into the enterprise cloud security market will allow it to enter another double-digit top-line growth phase it previously had in late 2016. Looking at both its current progress in the enterprise cloud security market and the overall opportunity space, we believe that Akamai can potentially double up its share price at the best case over the next two years.

As venture investors, we understand and like this business a lot. However, the technology part of it is quite challenging to execute without the right team. Since it started, Akamai has been a founder-led company, has never spent any single quarter unprofitable, and has established a competitive moat given its well-established networks across 253,000 servers in 137 countries.

Where Akamai is at

Akamai has spent the last 20 years in the business as a CDN (Content Delivery Network) company serving enterprise clients. CDN is pretty much a technology that enables online businesses to reduce the overall load time when serving contents to their users worldwide. Its clients include Facebook (NASDAQ:FB) and Airbnb (AIRB), which leverage Akamai servers in proximity to their users to serve their requests on almost all devices worldwide. 15-30% of all worldwide internet traffic today is delivered through Akamai CDN technology.

(Source: stockrow. Akamai's key metrics)

With over $1 billion in operating cash, $2.7 billion in revenue, and also double-digit net profit margin, Akamai is a valuable technology giant. Across the board, its TTM top-line growth has declined from 9.9% to 6.89% between 2016 to 2018. The reason behind the decline is that its core enterprise CDN business is declining in general. As per its Q2 2019 10-Q earnings call, one of the covering analysts brought this up:

.... you obviously mentioned the growth with the Internet Platform Customers on that CDN side. I'm just wondering if you could talk a little bit about, the trends in the business ex-the big 5. With that segment being down, I think it was 2% year-over-year this quarter and down 2% last quarter.

With only around 1% to 2% YoY growth seasonal upside when we exclude its 5 largest clients, there seems to be not much headroom for growth in the CDN market. There are opportunities in niche spaces that Akamai currently does not serve. In these spaces, we have seen players like Cloudflare, Fastly (NYSE:FSLY), or MaxCDN. As it stands, Akamai has been more interested in seizing the opportunity in the enterprise cloud security market.