Summary

- Investors and analysts love to make dramatic pronouncements based on quarterly earnings reports.

- One quarterly earnings “miss” or decline in revenue can overshadow years of steady profit growth.

- Despite these short-term concerns, this company’s long-term profit growth remains strong.

- Looking for more? I update all of my investing ideas and strategies to members of Value Investing 2.0 . Get started today »

Investors and analysts love to make dramatic pronouncements based on quarterly earnings reports. One quarterly earnings "miss" or decline in revenue can overshadow years of steady profit growth.

We first made this stock a Long Idea in November 2017, and it has outperformed the S&P 500 (up 21% vs. S&P up 16%) since then. However, the company's revenue and GAAP earnings have been hit by currency headwinds and non-recurring expenses over the past year. CNBC recently declared the company "in turnaround mode." Despite these short-term concerns, this company's long-term profit growth remains strong. Kimberly-Clark (KMB) is this week's Long Idea.

Accounting Earnings Hide Profit Growth

When we made KMB a Long Idea in 2017, we focused on the company's steady profit growth. KMB has grown after-tax operating profit (NOPAT) by 2% compounded annually over the past 15 years.

2% growth might not be exciting, but the reliability of the company's cash flows makes it appealing. Even in the midst of a recession in 2008, KMB's NOPAT declined by less than 5%. No matter the health of the economy, people always need tissues and diapers, and KMB makes money.

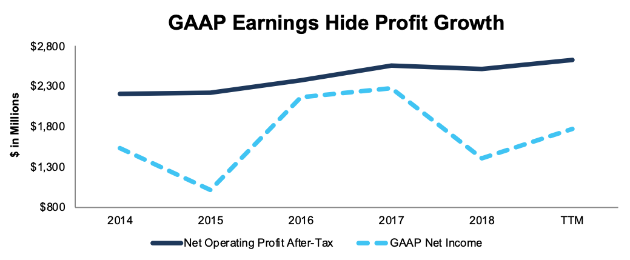

Investors who only look at accounting earnings might not appreciate the reliability of this company's profits. As Figure 1 shows, GAAP net income has been volatile in recent years even as NOPAT has continued its steady upward trend.

Figure 1: KMB's GAAP Net Income and NOPAT Since 2014

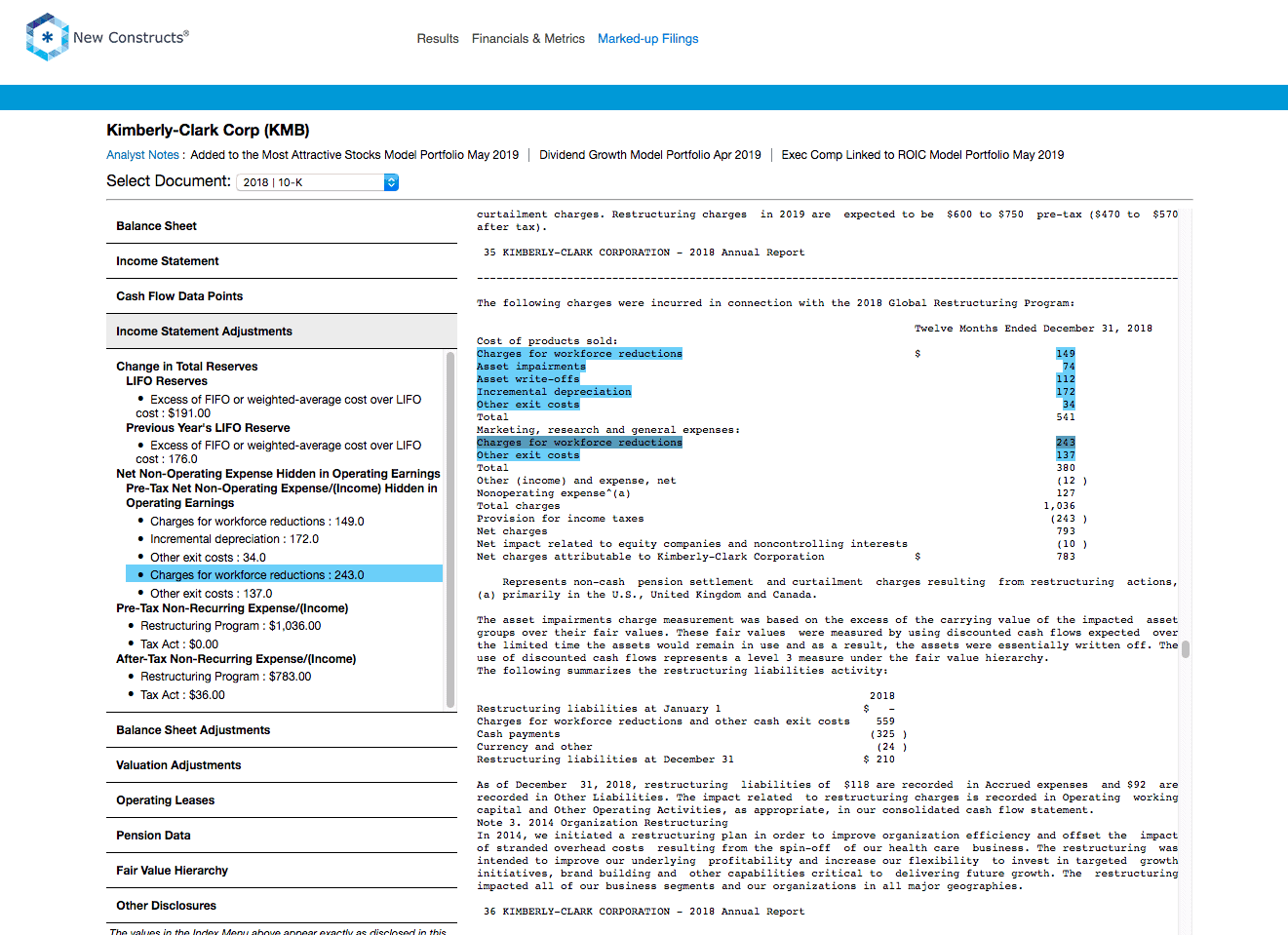

Four main items account for the disconnect between GAAP earnings and NOPAT in 2018:

- $735 million (4% of revenue) in one-time charges due to the company's cost-saving program, mostly related to layoffs

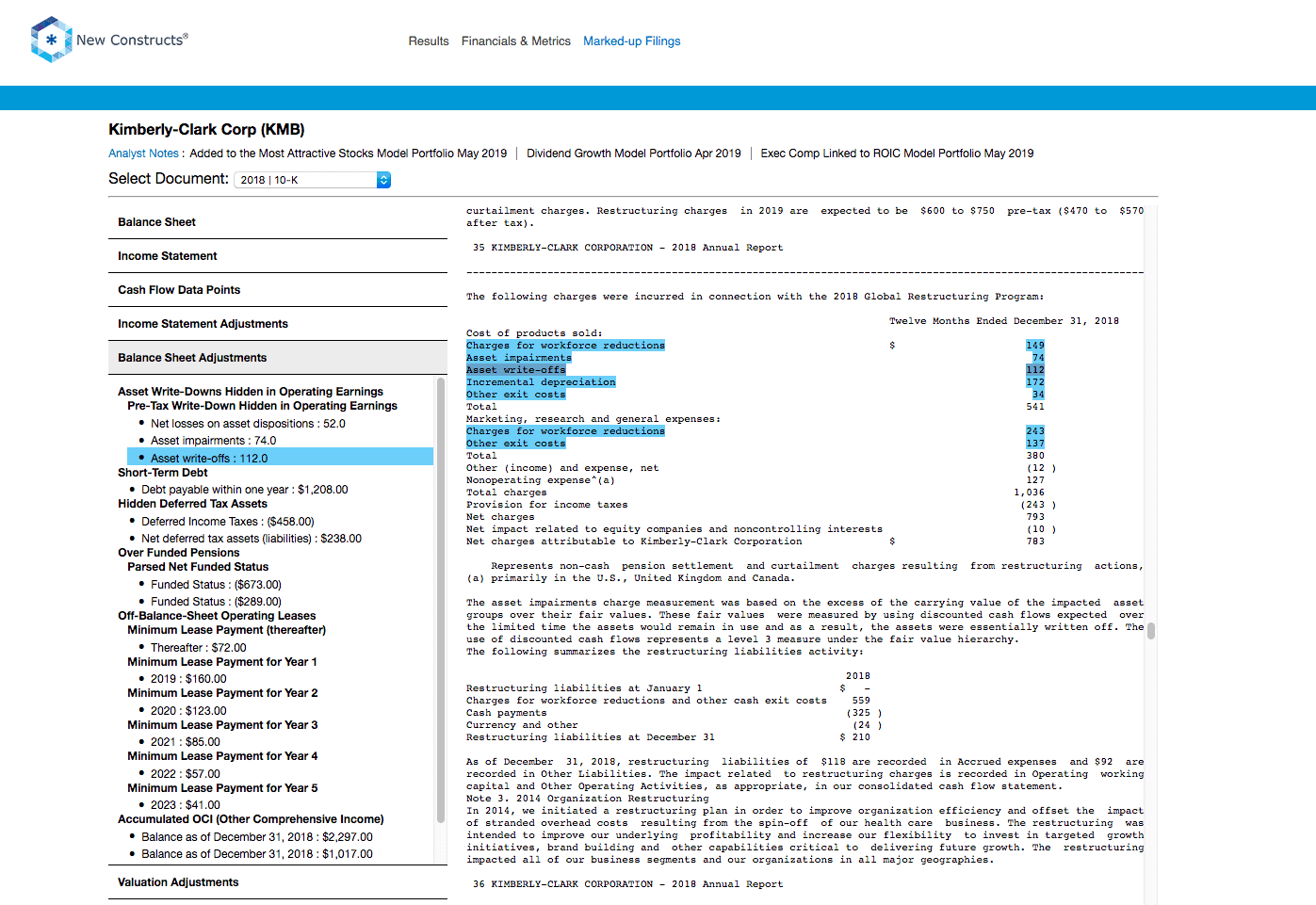

- $238 million (1% of revenue) in write-downs

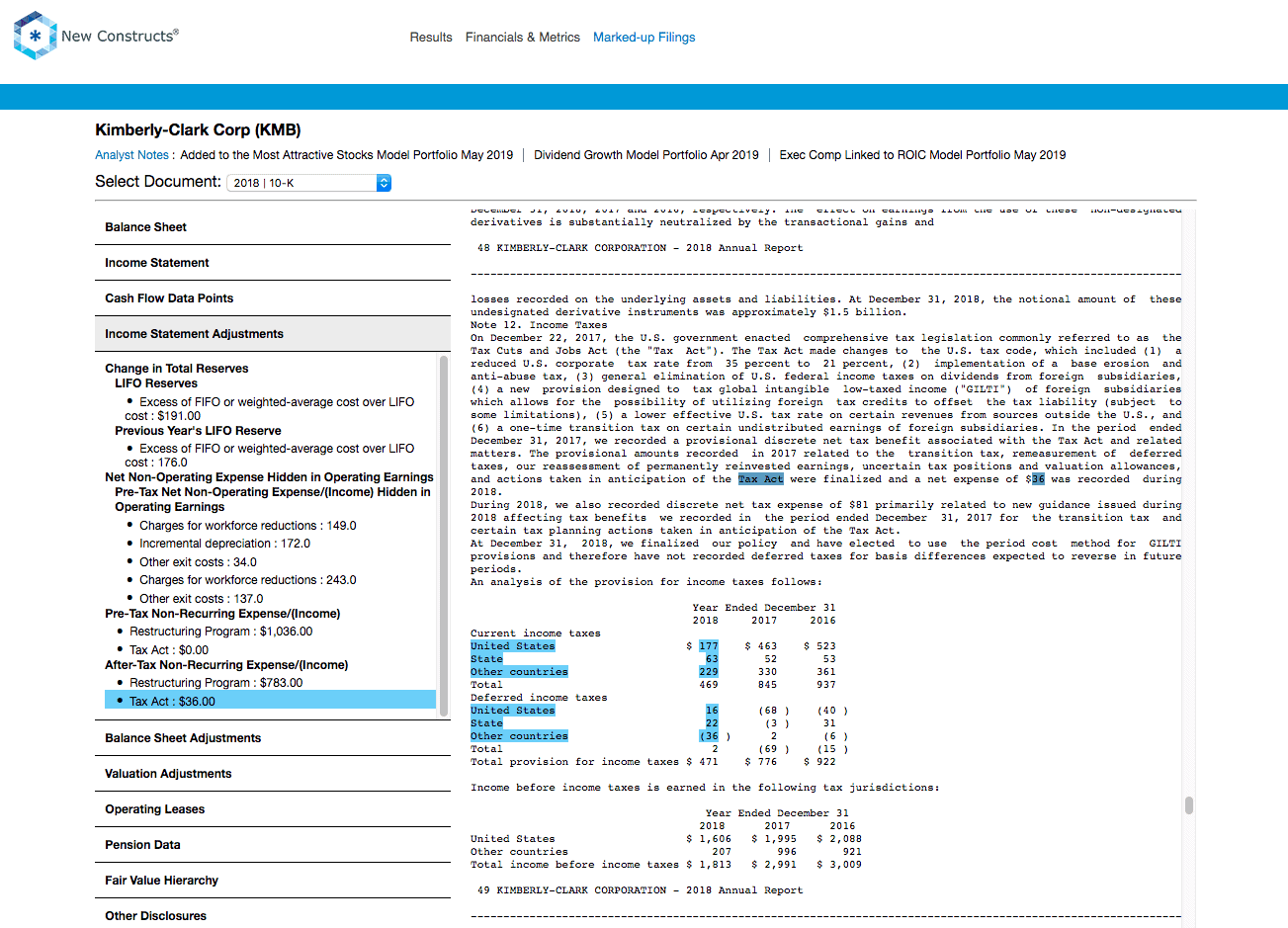

- $36 million in charges due to tax reform

- $15 million in increased LIFO reserves

All told, these unusual items led to a 38% decline in GAAP net income in 2018 even though NOPAT declined by just 2%.

Organic Sales Growth Looks Strong

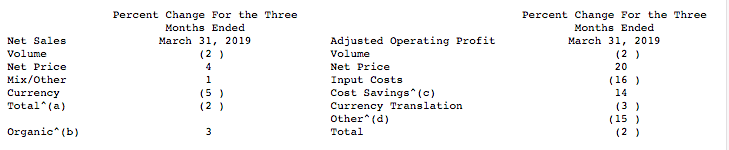

As Figure 1 shows, GAAP earnings bounced back in Q1 2019, but investors are still concerned over the company's 2% year-over-year (YoY) revenue decline. Cost cutting can only drive so much profit growth if revenues are shrinking.

However, a deeper dive into KMB's 10-Q shows that the underlying trends in the company's business still look good. Organic sales actually increased by 3%, driven largely by price increases. The revenue decline came entirely from a 5% foreign exchange headwind as currencies in Latin America depreciated against the dollar.

Longer-term, the company's increasing invested capital turns(revenue/average invested capital) show that KMB is improving its asset efficiency. Figure 2 shows KMB has a significant and growing advantage over the peer group listed in its proxy statement when it comes to capital turns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}