Summary

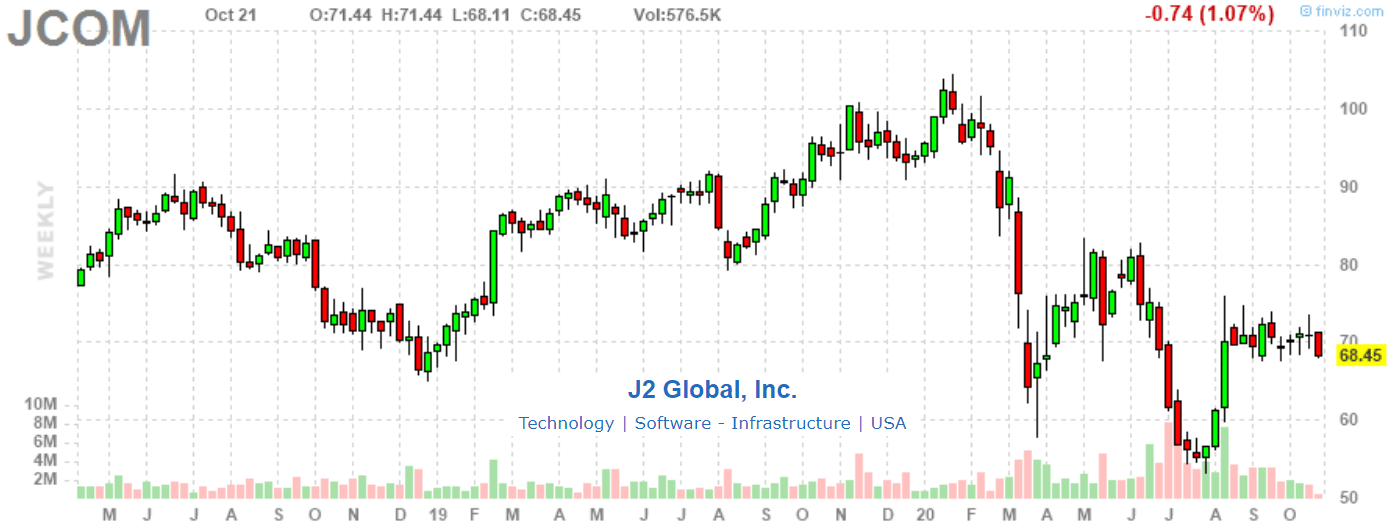

- Shares of J2 Global have been under pressure despite a resilient operating and financial environment this year.

- The company generates significant free cash flow, which supports a new share buyback program that yields over 20% through 2025.

- While the outlook for near-term growth is modest, the fundamentals are strong, and we like the attractive valuation and see upside in shares through next year.

- Looking for more investing ideas like this one? Get them exclusively at Conviction Dossier. Get started today »

J2 Global Inc. (JCOM) is an internet services provider with an extensive portfolio of digital media and cloud-based service companies. Website brands like IGN, PCMag, and Mashable, among others, are recognized as market leaders with a global audience. The services and subscription business includes tools like online fax services, VPN, and e-mail security applications used by both consumers and commercial customers. While certain parts of the business have seen disruptions due to the pandemic this year, the overall financial profile remains solid with steady growth and strong cash flows. We are bullish on shares that offer attractive value heading into the upcoming Q3 earnings release scheduled for November 2nd. This is a high-quality stock with a positive long-term outlook.

(Source: Finviz)

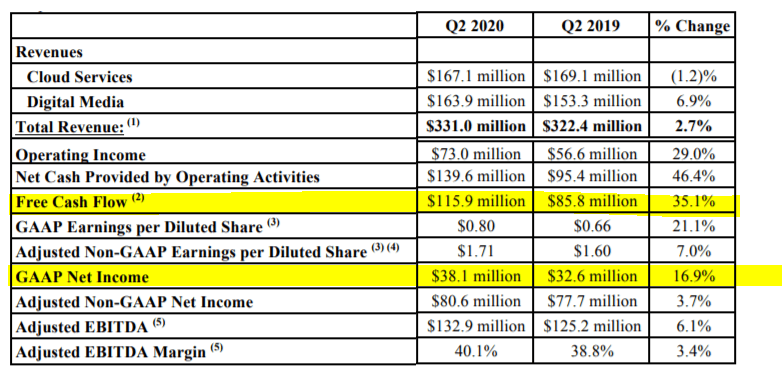

JCOM Financials Recap

In line with broader trends in technology companies, J2 Global's operating environment has been relatively resilient despite the pandemic. In the last-reported quarter, total revenues climbed by 2.7%, while adjusted EPS was 7.0% higher compared to the period in 2019. Notably, the adjusted EBITDA margin was up 340 basis points to 40.1%, driven by some cost-saving initiatives and the revenue mix. The positive earnings environment generated $116 million in free cash flow, up 35% y/y, a quarterly record for the company.

(Source: Company IR)

In terms of the operating segments, 6.9% y/y growth in digital media revenue was supported by strength in online advertising, which surprised management, as they had expected more weakness due to the pandemic. On the other hand, cloud services, which include various subscription-based businesses, saw revenues decline by 1.2%. The average monthly revenue per customer at $13.66 fell 2.5% y/y.