- I believe the margin should rebound nicely over the next couple of quarters.

- Profitability levels are likely to have bottomed in the second quarter and should improve materially over the next year.

- I believe that the credit concerns currently weighing on the stock are likely to prove too draconian.

Investment Thesis

Headquartered in Los Angeles, California, Hope Bancorp, Inc. (HOPE) is a $17.2 billion asset holding company and parent to Bank of Hope. Interestingly enough, HOPE is actually the only large scale community bank that is Korean-American focused. It has a pretty diverse lending set with a clear emphasis on commercial real estate and SBA lending. It has offices all over the United States; more specifically branches are located in Alabama, California, Georgia Illinois, New Jersey, New York, Texas, Virginia, and Washington State, along with having an office in Seoul, South Korea.

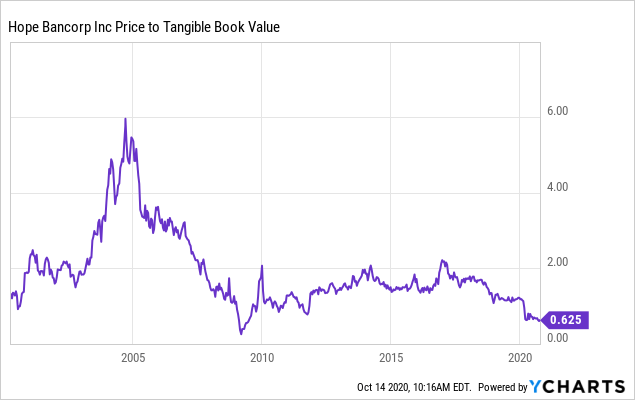

I completely understand why HOPE trades at a discount to peer banks given its past credit problems. Most peer mid-size community banks are trading at 1.1x price to tangible book value per share. As one can see from the chart below, HOPE currently trades at a 40% discount to that. My bullish stance on the shares is based on the current valuation being too low relative to peers.

Fundamentally, I believe HOPE has appropriately built up its loan loss reserve enough to warrant a roughly peer like valuation. I think the credit profile does give people caution, which I understand. However, my argument is that HOPE has already positioned itself to sustain above average losses. In my mind, the share price should be much closer to peers.

Data by YCharts

Data by YChartsRevenue Outlook

The second-quarter spread revenue came in at $109.8 million, marking a roughly $10 million decrease relative to the first quarter. Based on my analysis, I found that the net interest margin (NIM) accounted for the entirety of the linked quarter decrease. The second quarter reported NIM was 2.79% relative to the first quarter’s 3.31% margin. Total loans increased $275 million while deposits increased $1.3 billion.